Turn regulatory complexity into a human-centered experience, showing enterprise-level strategic thinking across three touch points.

The Challenge

Section 1

Dashboard UX

Front End UI

Back End Data Systems

Take a cluttered data dump and re-org with applied IA principles to prioritise key metrics.

Understand API constraints and latency through the developers eyes, ensuring the UI is designed gracefully while loading large datasets.

Goal

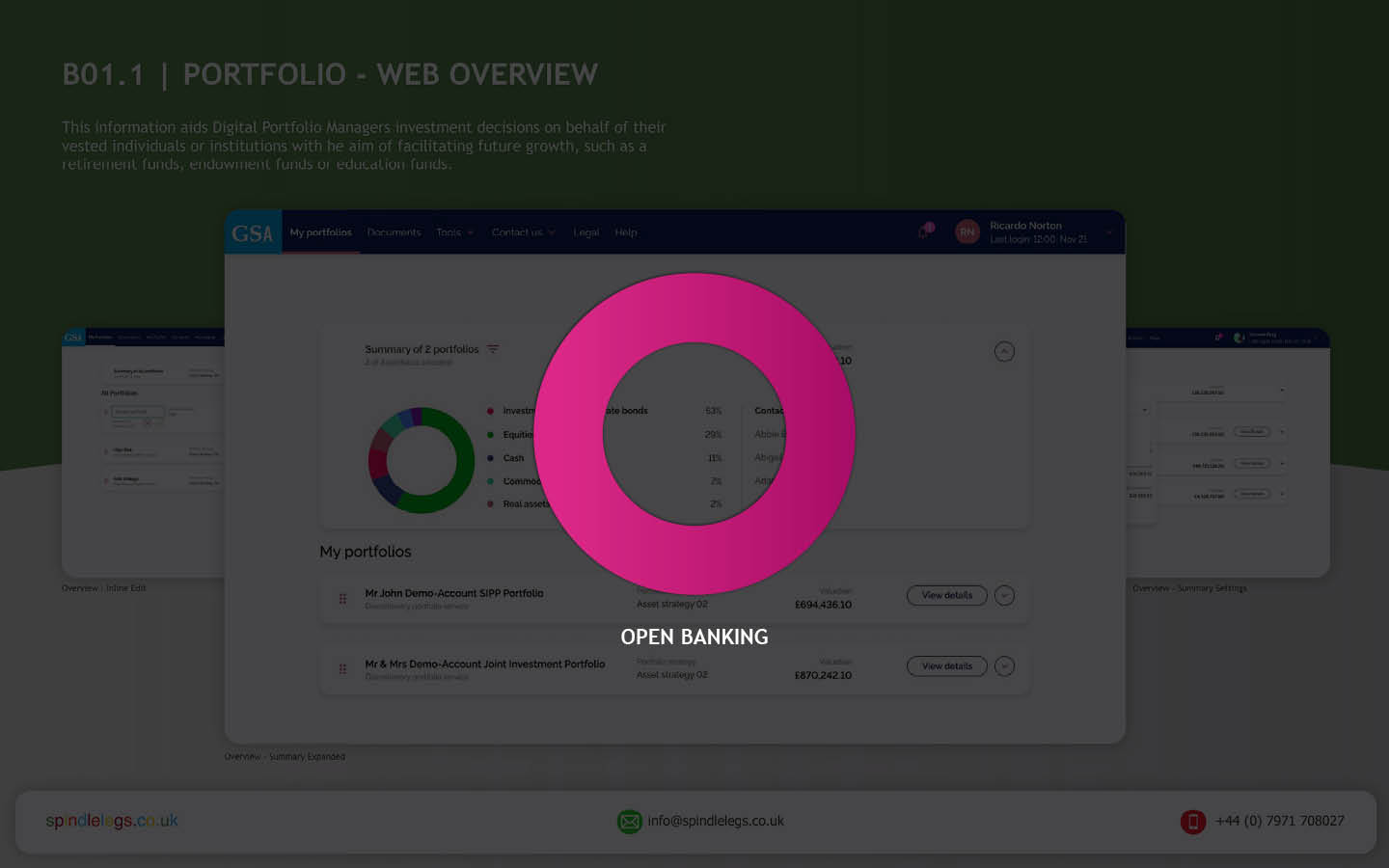

Implement the Account Information Service Provider (AISP) flow for Open Banking on desktop. Provide users with aggregated financial insights within a complex data Dashboard from multiple sources.

Secondary Goal: Demonstrate strong understanding of FE interactive design solutions for BE data systems.

The Problem

Open Banking consent is inherently complex and intimidating, leading to high drop-off rates and regulatory fines.

Strategic Opportunity: Design a Consent Management Dashboard that not only meets legal requirements (i.e. PSD2, CMA) but also builds trust, by making the flow transparent and effortless.

Business & User Goals

User Success Metric: Allow users to manage their third-party connections with confidence and clarity.

Gathering the principal players

This case study hinges on transforming a fragmented jigsaw of data into cohesive, high-trust UX that fosters familiarity and security.

UX Writing

AI UX Designer

Data Points

Thinking entity to symbolise Open Banking

This AI-UX designer employs the hybrid model:

Human

Journey designing, API and BE driven integrations, and user needs

A simple AI prompt

Create an abstract amorphous image, a ‘thinking’ entity for a financial dashboard using gradient blues and green

Navigation

An action-oriented, collapsible side nav needs to balance financial utilities (i.e. linked accounts and permission-driven consent) while managing who has access to what.

To respect confidentiality agreements, the branding and specific naming have been modified. This product is currently live and serving 10K plus HNW users.

Defining the Gold Standard Row Content

API > Actionable

Prompt; Nano Banana

Shift the data from static information to high-trust insights. By balancing security indicators (timestamps, verified credit boost), the interface transforms complex Open Banking API calls into a true financial dashboard.

Prototyping & Flow Design

Section 2

Active consent

Data transparency

Design to steer strategy and make complexity feel simple.

Revoking Permissions

Progressive disclosure

Dashboard UX

Iconography

Financial dashboard

This Linked Accounts UI moves beyond a simple list of connections, transforming a technical req. into a high-value financial dashboard.

Design Solution

Revoke: A two-step confirmation modal

- Clearly show what is next

- Demonstrate consequences (i.e. “You will lose access to X)

- Keep the user informed

Prototyping

Goal

Introduce a clickable mid-fidelity prototype to define a concise, step-by-step journey, using a Just-in-Time disclosure model to manage information overload.

Re-connect (or re-authorise)

AISP Flow

ACCOUNT Sharing

Micro-interactions

The Off-Ramp

Simplifying the renewal process with an option to “Revoke” with a single click.

Design Solution

What data is being shared

Which account

Confirmation

Consolidate Account Identity with real-time Transactional Intelligence. Transform fragmented data into a clear feedback that surfaces categorised spend and Live Balances for smarter budgeting.

Prototyping

Goal

Discover unwanted connections, show transparency by surfacing shared information

and provide control by allowing for a clear account selection process.

Lessons Learnt & Outcomes

Section 3

DATA retention

Human-readable insight

The Just-in-Time Model

Cognitive overload

Data retention

Revocation & Renewal

The Takeaway: The “Off-Ramp” (revocation) is just as important for trust as the “On-Ramp” (onboarding). A Progressive Disclosure model for revoking permissions prevents information overload.

- Outcome: A two-step confirmation modal for revocation.

- Opportunity: Separating expired consents (< 90 days) from older data (> 90 days) could better inform users about long-term data retention policies.

High-Trust UX

Dashboard UX

Security

Using IA to instil trust

The Takeaway: Consent shouldn’t feel like a legal hurdle. It should feel like a security feature. By moving away from a data dump to applied IA, the complexity of PSD2/CMA requirements is rebranded as a transparency benefit.

- Outcome: Gold Standard Row Content model that translates technical API calls into human-readable insights.

- Opportunity: Logical Chunking can reduces cognitive friction, adding a I do not recognise flow with Fraud warning capability goes that extra step.

![]() Figma Tip: Vertical v Horizontal

Figma Tip: Vertical v Horizontal

Component variants: Designing a data-rich responsive Figma table row and cell components with auto-layout should be set-up with component variants, giving the flexibility to swap in complementary formats for differing data points.

Cell Design: For the ultimate flexibility, component cells should be stacked in a vertical AL column, set to (W) Fill.

Outcomes

The project proved that prioritising transparency and control in regulatory design is the highest leverage move. Focus on clear FE design, BE clarity, and the details (i.e. 90 day consents) to transform a legal requirement into a trust-building feature.

Go Beyond the Screenshot

Static frames only tell half the story. To truly understand the user journey, to feel the interaction several high-fidelity Figma prototypes are available for walkthroughs.

Advanced prototyping

Auto Layout

Microinteractions

Design Systems

Please get in touch and request access